The semiconductor industry is the backbone of numerous technological advancements, serving as the foundation for sectors ranging from artificial intelligence (AI) and electric vehicles (EV) to consumer electronics. As global demand for technology continues to surge, the semiconductor landscape is experiencing profound transformations. These shifts are shaped by technological innovation, market forces, and geopolitical considerations. This analysis delves into the current state of the semiconductor sector, exploring the challenges it faces and assessing its future outlook based on insights from recent industry reports.

The current state of the Semiconductor Industry

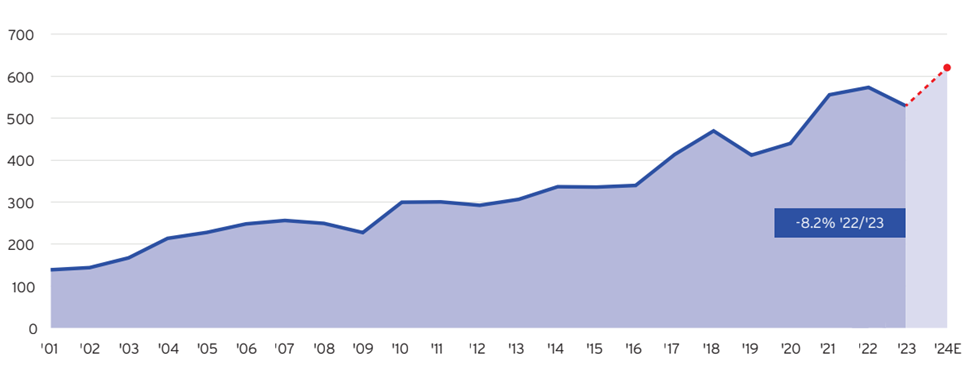

The semiconductor industry appears positioned for substantial growth. The industry is projected to reach global revenues of $611 billion in 2024, a 16% increase compared to 2023. By 2030, the market is expected to exceed $1 trillion in sales. One key growth driver is AI accelerators, which are anticipated to generate around $400 billion in revenue by 2027. These accelerators play a crucial role in powering AI algorithms in data centers, cloud computing, and edge devices.

The demand for AI chips is expected to continue increasing as companies across industries integrate AI into their operations, further solidifying the role of semiconductors in driving future technological innovation.

Global Semiconductor Sales ($B)

Source: SIA

Challenges facing the industry

While the outlook for the semiconductor industry remains optimistic, there are significant challenges that companies within the industry must navigate.

Supply chain disruptions

One of the most prominent issues is the ongoing supply chain disruptions. The COVID-19 pandemic exposed vulnerabilities in the global semiconductor supply chain, leading to chip shortages that have impacted industries worldwide. Although efforts are being made to diversify and strengthen supply chains, challenges persist due to the complex, global nature of semiconductor production.

Geopolitical tensions

Geopolitical tensions between the US and China also add layers of complexity. With the US imposing export restrictions on advanced semiconductor technologies, China has intensified efforts to build its domestic semiconductor industry. This geopolitical competition is reshaping global supply chains and is likely to impact market dynamics in the coming years.

China’s market share in mature-node semiconductor manufacturing is projected to increase substantially, which could lead to increased competition and potential price wars in certain segments.

Technology limitations

Another challenge involves the physical limitation of semiconductor technology itself. As chip manufacturers push to develop smaller, more powerful chips, they are approaching the physical boundaries of how small transistors can be manufactured.

Currently, advanced semiconductor packaging technologies, such as 3D packaging and system-in-package (SiP) solutions, offer ways to extend performance without relying on further transistor miniaturization. These advanced packaging techniques are expected to rapidly grow in relevance, especially for applications in AI and high-performance computing (HPC), as they allow for the integration of multiple chip types within a single package.

Future prospects

Looking ahead, the future of the semiconductor industry appears robust, underpinned by sustained demand for advanced technologies in AI, automotive, and telecommunications. AI, HPC, and electric vehicles are projected to drive semiconductor sales through 2030. AI chips should continue to be a major growth driver as more industries adopt AI for automation, data analysis, and decision-making. Meanwhile, the automotive sector will remain a key growth area as EV adoption accelerates globally.