Happy Sunday to everyone on The Street.

You asked, we answered.

We ran a special “Equity Research” edition of our newsletter ahead of the election, and asked you, our readers, whether you’d like more in the future. The response was a resounding, “Yes.”

So, as promised, we’re interrupting your usual Sunday programming once again with a deep dive into a stock that may be impacted by the upcoming holidays.

If you missed last week’s report, check it out here.

And before we dive into today’s, here’s a quick word from our sponsor:

Sponsored By Mode Mobile

Mode Mobile is flipping the script on smartphone use. While others drain your wallet, Mode's EarnPhone fills it. Their EarnOS platform has helped 45M+ users earn and save over $325M. Now Mode is targeting the global market of 7B+ smartphone users backed by retail giants and 28,000+ savvy investors.

This is a paid advertisement for Mode Mobile Regulation A offering. Please read the offering circular and related risks at invest.modemobile.com.

Party Like It's 2009

Has a single stock seen a wilder Cinderella Story in recent years than Abercrombie & Fitch (ANF)?

(And, no, not just because its infamous ads scream “NSFW Prince Charming”.)

Abercrombie — and its unmistakably pungent cologne — was a dominant mall brand back in the aughts. Then, in the early 2010s, mismanagement and controversial comments by then-CEO Mike Jefferies sent the brand into a downward spiral.

The story didn’t end well for Jefferies, who was indicted on federal sex trafficking charges back in October. But it’s practically a fairy tale for the once-maligned brand.

Since 2023, ANF’s stock is up more than 600%, thanks largely to extensive restructuring and rebranding efforts. Gone are the short-shorts and muscle tees, replaced by trendier knit polos and high-rise jeans. But in terms of relevance and performance, ANF has been partying like it’s 2009.

Can that momentum last through this holiday season?

Let’s dive in.

Executive Summary

Analysts widely acknowledge Abercrombie & Fitch’s improved inventory management, rising profit margins, and strong brand appeal as critical drivers. Of 9 analysts covering the stock, 5 rate it a Hold, 3 a Buy, and 1 a Strong Buy. Its average 12-month price target is $185, indicating an upside potential of 22.5% from its current price of $151. ANF has also delivered a more than 100% trailing 1-year price return.

These metrics highlight confidence in the company’s ability to execute its “2025 Always Forward Plan,” which emphasizes store optimization, geographic expansion, and digital growth. The company’s robust cash position and underpenetrated international markets suggest some long-term potential too.

However, some market observers lean cautious on the stock, due to macroeconomic risks and decelerating H2 FY2024 growth. Valuation concerns also persist, as ANF trades at a slight premium to peers.

Company & Industry Overview

Founded in 1892 and headquartered in New Albany, Ohio, Abercrombie & Fitch is a specialty retailer offering casual apparel, accessories, and personal care products.

Operating under two main segments — Hollister and Abercrombie — the company boasts approximately 729 retail stores across Europe, Asia, Canada, the Middle East, and the US, complemented by robust e-commerce and third-party licensing channels.

Abercrombie & Fitch holds a competitive 7.7% share of the US apparel market, positioning it alongside key rivals like Gap Inc. (8.5%) and American Eagle Outfitters (6.2%).

The global apparel industry is forecasted to grow at around 4% CAGR through 2028.

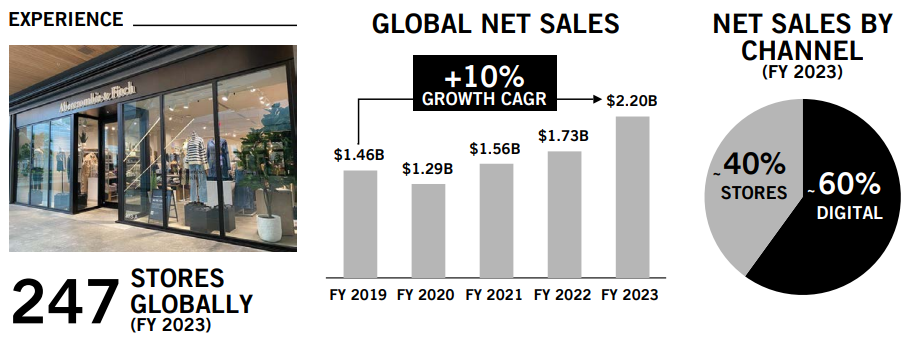

Abercrombie Brands

Source: Company Presentation

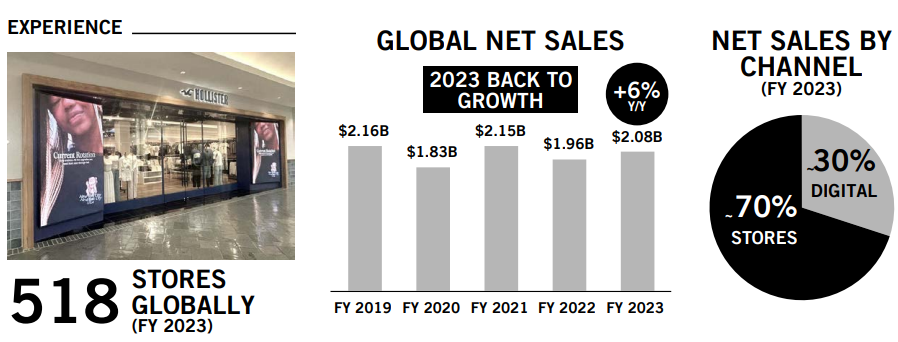

Hollister Brands

Source: Company Presentation

The Bull Case

It’s hard not to be impressed by the run Abercrombie & Fitch has had in recent years. The question for investors is how long it can continue.

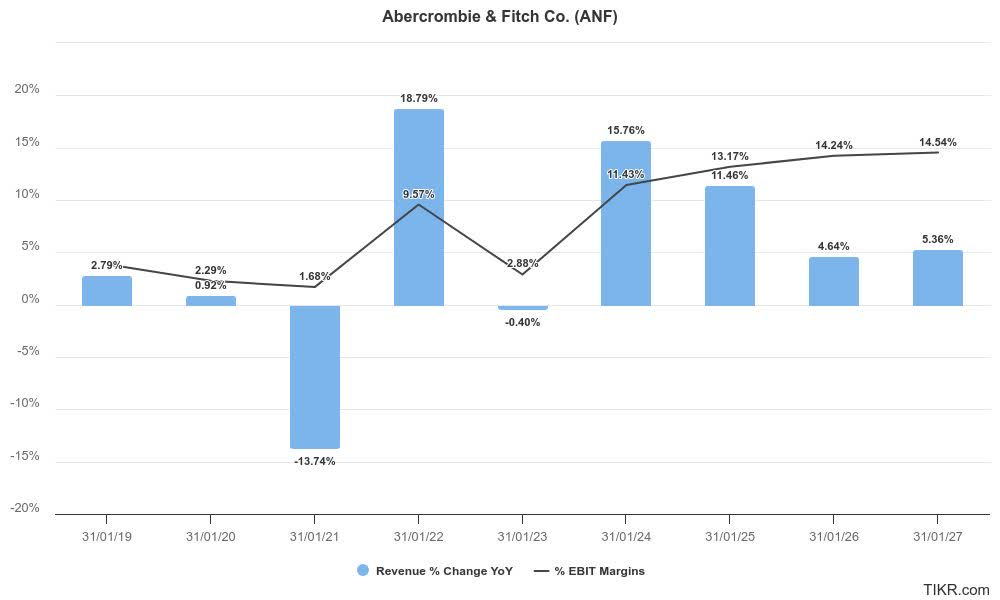

For the bulls, confidence stems from the company’s robust cash position ($738 million) and lack of long-term debt. Furthermore, despite the broader retail market’s volatility, comparable store sales at Abercrombie and Hollister brands have grown 26% and 17% year-over-year, respectively. This signals ANF’s impressive ability to navigate shifting consumer preferences, fueled by targeted digital and social marketing.

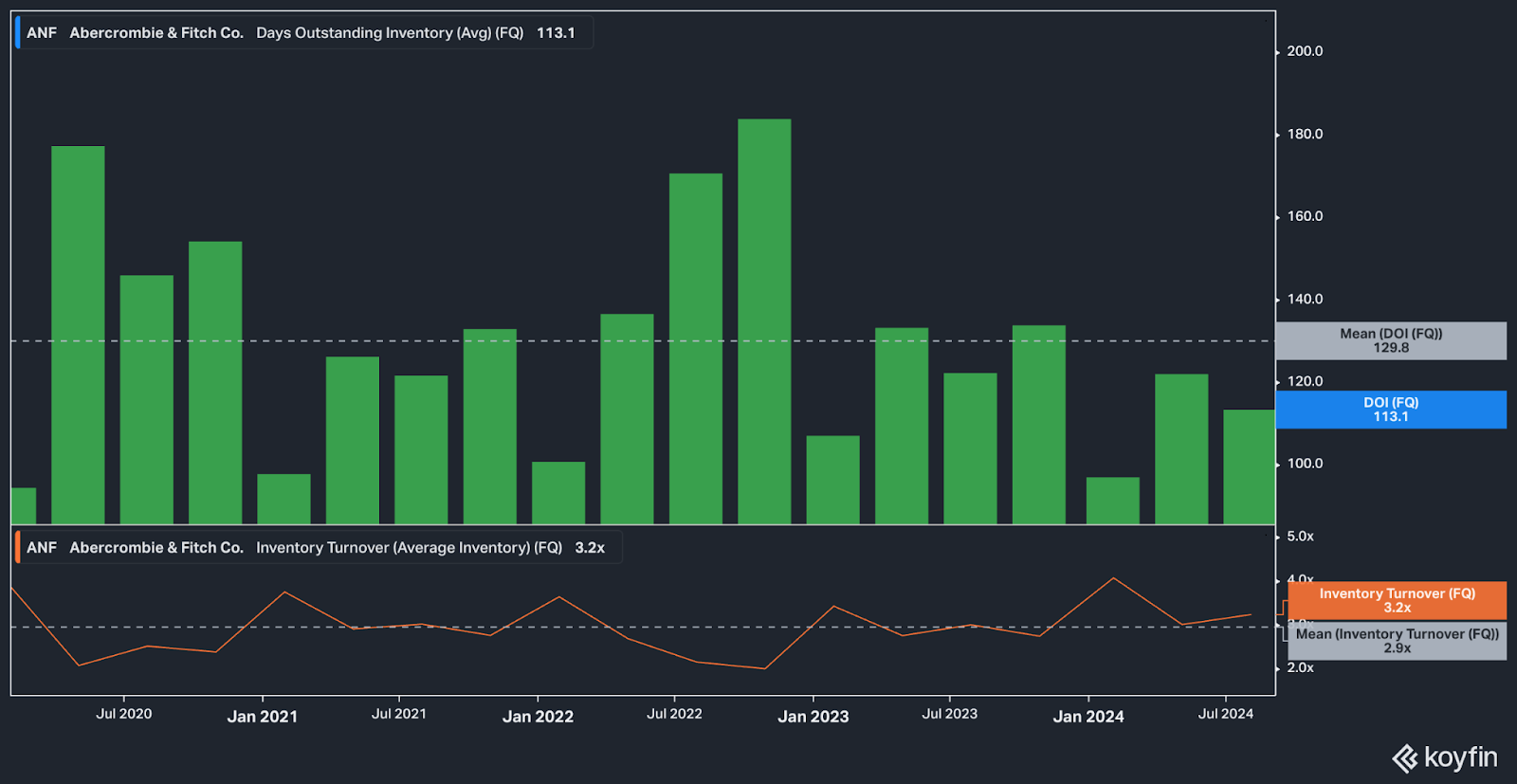

Bullish analysts also commonly highlight ANF’s efficient inventory management, a critical factor in retail, supporting higher margins and improved cash flow.

Abercrombie’s Improving Inventory Management

Source: Seeking Alpha, Koyfin

Potential long-term growth catalysts include ANF’s targeted geographic expansion, particularly in Europe and APAC, where a roughly $400 million revenue opportunity remains underpenetrated.

Additionally, bulls view ANF’s margin improvement efforts as promising. The company’s gross margin reached 63.6% in H1 2024. Continued execution of strategic initiatives, alongside market-leading profitability improvements, may position ANF favorably for sustained earnings growth and positive investor sentiment.

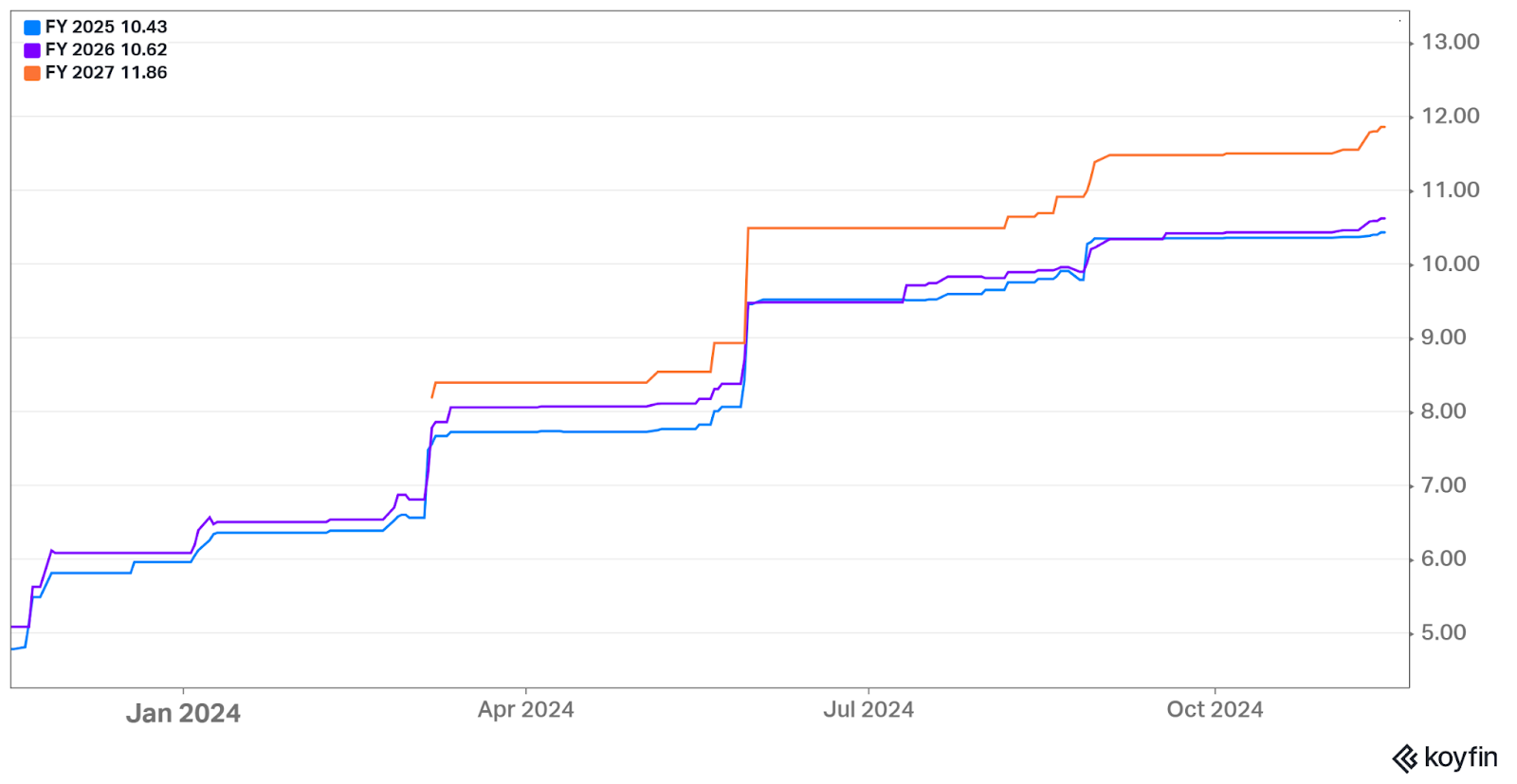

Uprising Consensus On EPS

Source: Koyfin

The Bear Case

Bears have several reasons for a more cautious approach to Abercrombie & Fitch, particularly its exposure to cyclical and unpredictable retail dynamics. ANF operates in a highly competitive and trend-driven industry. Bears argue that the company’s rapid resurgence could just as easily turn into a speedy descent.

Macroeconomic headwinds further compound these risks. As a retailer of discretionary goods, ANF is highly vulnerable to a potential downturn in consumer spending.

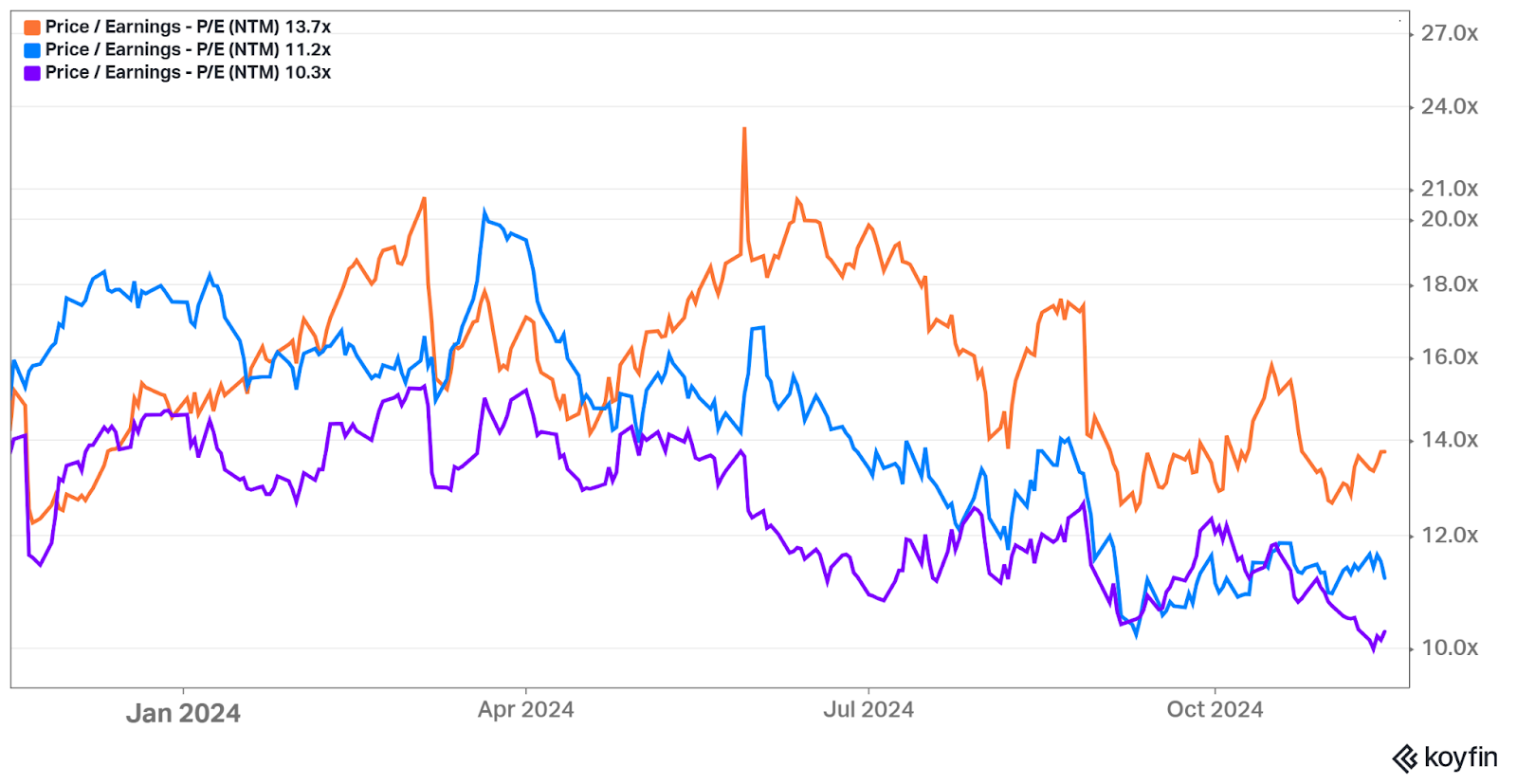

Valuation concerns also weigh on the bearish outlook. ANF's share price saw a more than 70% total return YTD, and it currently trades at a forward price-to-earnings (P/E) ratio of 13.7x, a premium to competitors like Gap (11.6x) and American Eagle Outfitters (10.2x).

Furthermore, the company’s high operating margins could face pressure if input costs (like cotton) rise or freight costs remain elevated, underscoring the risks of relying on cost efficiencies to sustain profitability in a volatile retail environment.

Financial Analysis & Valuation

Abercrombie & Fitch has demonstrated strong financial performance in FY2024, delivering record results in the third quarter, with adjusted earnings per share (EPS) surging 36.6% annually. Net sales also rose 14%, marking the sixth consecutive quarter of double-digit growth. Both readings beat consensus expectations on the Street.

Consensus Estimates

Source: TIKR, Seeking Alpha

Despite ANF’s high P/E relative to its peers, its EV/EBITDA multiple stands at 6.3x (based on FY2024 estimates), aligning more closely with industry norms and suggesting that the stock may be fairly priced after all.

Last Year P/E Multiple (Forward Year): ANF vs Competitors

Source: Koyfin

ANF’s valuation appears justified by robust growth metrics, operational efficiency improvements, and rising revenue estimates, which analysts have revised upward to $4.82 billion for FY2026.

Meanwhile, forecasts of decelerating growth in H2 FY2024 did not materialize in Q3, suggesting the company could indeed continue its record run into the ever-important holiday season.

While the stock is far from undervalued, and high investor expectations may warrant caution, Abercrombie & Fitch still appears attractively priced for its growth trajectory and operational discipline, and merits a close look from prospective investors.

Sponsored By Mode Mobile

Mode Mobile is flipping the script on smartphone use. While others drain your wallet, Mode's EarnPhone fills it. Their EarnOS platform has helped 45M+ users earn and save over $325M. Now Mode is targeting the global market of 7B+ smartphone users backed by retail giants and 28,000+ savvy investors.

This is a paid advertisement for Mode Mobile Regulation A offering. Please read the offering circular and related risks at invest.modemobile.com.

This message is a paid advertisement for Mode Mobile. The Street Sheet (SS) receives a flat fee from Mode Mobile totaling up to $4,500. Other than the compensation received for this advertisement sent to subscribers, The Street Sheet and its principals are not affiliated with Mode Mobile. This advertisement is sponsored by a third-party Reg A crowdfunding issuer and is for informational purposes only. The Street Sheet does not endorse or recommend any specific offering, and this advertisement should not be construed as a recommendation to invest. Investing in securities, including those offered through Reg A crowdfunding, involves risk, including the potential loss of principal. These investments are speculative, illiquid, and may involve a higher degree of risk compared to more traditional investments. The Street Sheet has not verified the information provided by the advertiser, and we encourage readers to conduct their own due diligence and consult with a licensed financial advisor or other qualified professional before making any investment decision. By engaging with this advertisement, you acknowledge that The Street Sheet and its affiliates are not responsible for any decisions or actions taken based on the information provided in this advertisement. All investments carry risks, and past performance is not indicative of future results. Readers should carefully review all information provided by the issuer, including the offering circular and any other available materials, prior to investing. The Street Sheet may receive compensation from the advertiser for promoting this offering. The Street Sheet and its principals do not own any of the stocks or shares mentioned in this email or in the article that this email links to. The Street Sheet is a research service not owned or managed by registered brokers and therefore this site does not make any investment recommendations. The information provided in this newsletter is not guaranteed as to the accuracy or completeness. Each user of SS chooses to do trades at their sole discretion and risk. SS is not responsible for gains/losses that may result in the trading of these securities. This newsletter includes paid advertisements. The source of all third-party content in which SS receives some sort of compensation is clearly and prominently identified herein as "ad", "Sponsored", or “Together With”. Although we have sent you these advertisements, SS does not specifically endorse any third-party product nor is it responsible for the content, the accuracy, or the completeness of the advertisement or the experience with the third-party advertiser. Furthermore, we make no guarantee or warranty about what is in the advertisement. All investments involve risk, losses may exceed the principal invested, and the past performance of a security, industry, sector, market, or financial product does not guarantee future results or returns. This communication from The Street Sheet is for informational purposes only. It is not intended to serve as a recommendation to buy, sell, or hold any security and is not an offer or sale of a security. Information contained within should not be perceived as a research report and is not intended to serve as the basis for any investment decision. Any third-party views reflected herein do not reflect the opinion of The Street Sheet. All investments involve risk and the past performance of a security does not guarantee future results or returns. There is always the potential for financial loss when investing in securities or other financial products. The information contained in this newsletter is subject to change without notice, and we do not undertake any obligation to update it. Readers are encouraged to conduct their own research and due diligence and seek advice from licensed professionals regarding their specific financial needs and circumstances. By reading this newsletter, you agree to hold us harmless from any and all losses, liabilities, costs, or expenses arising from your use or reliance on the information provided. There is no warranty as to the accuracy or completeness of the factual matters included in any advertisement or sponsored content in the newsletter. You have not performed any research on any entity, or its business, that advertises or submits any sponsored content. The Street Sheet is reader-supported. When you buy through links on our site, we may earn an commission.