Capitalizing on AI tailwinds

Super Micro Computer (SMCI) posted its financial results for F4Q24 in August, surprising investors with lower-than-expected gross margins. Despite this temporary setback, there are several reasons to be optimistic about the company's long-term growth, particularly as it leverages its leadership in AI and cloud infrastructure markets. This analysis delves into Super Micro's financial performance, margin challenges, and its outlook for fiscal 2025 and beyond.

Margin challenges: A temporary setback?

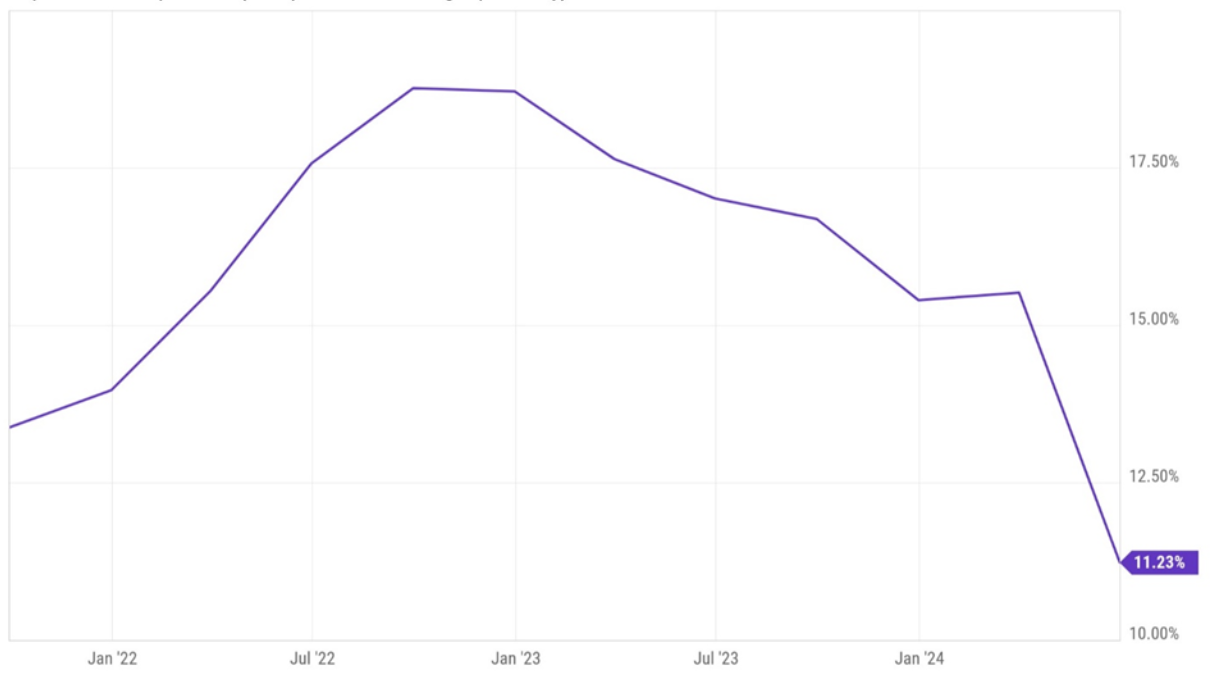

The key concern arising from Super Micro’s F4Q24 earnings report was its gross margin drop to 11.3%, well below its long-term target range of 14%-17%. This decline was attributed to inefficiencies in manufacturing liquid-cooled racks at scale, a relatively new process for the company. Furthermore, higher shipping costs compounded the margin pressures, particularly in the hyperscale AI server market, where fierce competition and a focus on cost control led to aggressive pricing concessions.

Despite these challenges, Super Micro expects margins to improve sequentially throughout fiscal 2025. With production inefficiencies gradually declining and the strategic ramp-up of its Malaysia facility, the company forecasts its gross margins to return to the low end of its long-term target by year-end. Additionally, a shift toward a higher mix of tier-2 cloud customers, which command less aggressive pricing, could further support margin recovery.

Super Micro Computer (SMCI) Gross Profit Margin (Quarterly)

Source: Ycharts

Growth catalysts: AI and cloud demand

Super Micro's strong position in the AI server market is a key growth driver. The company's $26-$30 billion sales guidance for fiscal 2025 underscores the robust demand for AI infrastructure, which is only expected to accelerate in the coming years. Despite delays in Nvidia's (NVDA) next-generation Blackwell GPUs, customers continue to invest heavily in current-generation solutions, particularly in liquid-cooled AI clusters.

Hindenburg's short report highlights valid concerns

While AI demand remains a solid tailwind, Super Micro must address its financial infrastructure challenges, which were highlighted in a recent Hindenburg short report.

Street Sheet Cheat Sheet: A “short report” or “short-sellers report” is a report indicating that a company has shorted a stock and the reason behind the short. This information typically raises investor skepticism, resulting in a selloff. Since investors might sell their positions after a short report is released, the short report author could further benefit from their short position on the stock. Because of the vested interest short sellers hold in the reported company, the report can often be interpreted as biased.

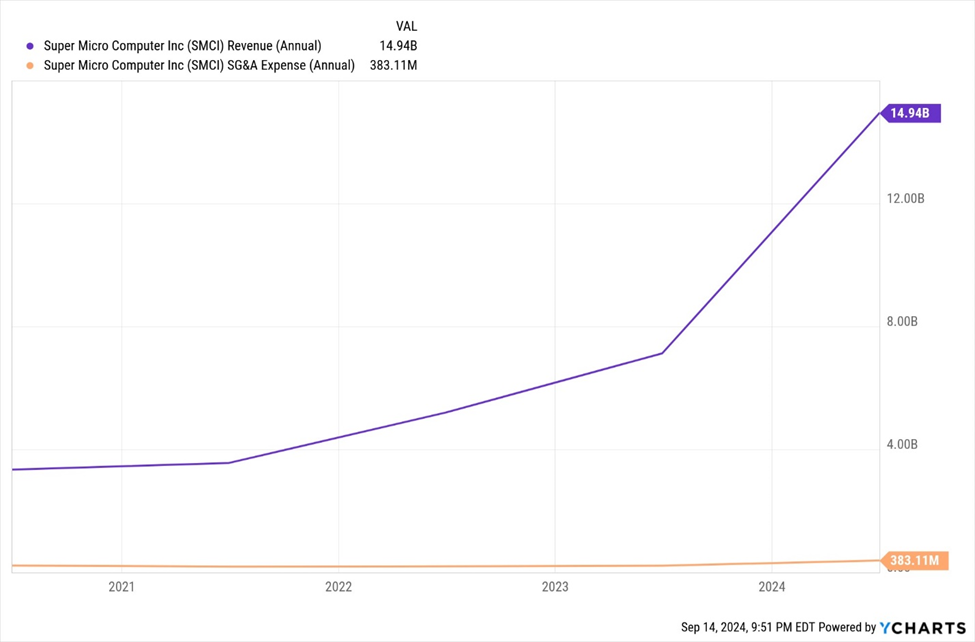

The Hindenburg report raised concerns about the company's accounting practices and delayed 10-K filing, which has introduced near-term uncertainty. However, these risks appear to be related to the company's inability to scale its financial controls in tandem with its exponential sales growth rather than any malfeasance. Sales have surged at a 61% compounded annual growth rate from 2021-2024, while general and administrative (G&A) expenses have only increased by 9% over the same period.

Super Micro Computer Revenue Growth Versus G&A Expense Growth

Source: Ycharts

Company Profile: SMCI

While Super Micro's near-term margin challenges are concerning, its long-term growth prospects remain intact, driven by strong demand in the AI and cloud markets. The company's ability to scale its manufacturing operations, secure high-value deals, and improve margins will be critical to sustaining investor confidence. As it navigates these challenges, Super Micro remains a "show-me" story, with its P/E multiple likely contingent on successful margin improvement.

This is perhaps why most Wall Street analysts currently have a hold rating on SMCI. Based on 16 Wall Street analysts who have issued ratings for Super Micro in the last 12 months, the stock has a consensus rating of "Hold." Of these analysts, 1 has given a sell rating, 10 have given a hold rating, and 5 have issued a buy rating.

As for the price targets, the average twelve-month price target is $790, with the highest price target being $1,500 and the lowest set at $325. This average price target suggests a 70% upside from the current price of $465.94.

Word on the Street: SMCI

The Street Says: HOLD | Consensus Price Target: $790 |

Sell: 1 Analyst Hold: 10 Analysts Buy: 5 Analysts |

|